Reader Question: I had a low appraisal. I recently closed on a home for $180,000. I just learned the appraiser along with the agent and lender adjusted the appraisal from $176,000 to $179,000. They never informed me of the original price. Had I been informed, I could have negotiated for the $4,000. What can I do now? Sonja D.

Monty’s Answer: Hello Sonja and thank you for your question. On the surface, one could interpret the actions of these providers as unacceptable or even unethical. However, with more detail about the circumstances and events leading up the adjustment it may play out differently. It is situations like this one, and many others, that add unseen complexity to real estate transactions.

There are considerations regarding who should have disclosed this information, or if there was an obligation to disclose.

Real estate law changes from state to state. The legal theories regarding ethics, disclosure principles and rules, case law and interpretation is complex. Conversations in some states between you and the real estate agent can create agency relationships. There can be a fine line between legal and moral issues, and often decisions are made on a judgment in the heat of the moment because the situation is not clear and an important deadline is looming.

Important points to consider

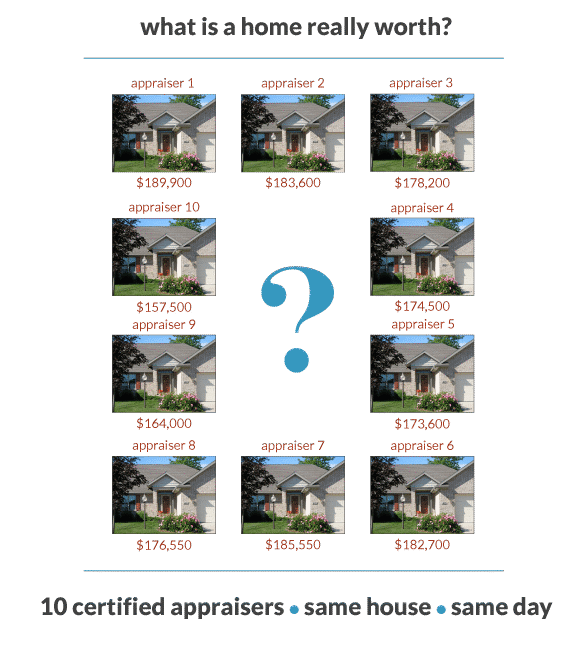

- The value of every home is a moving target. A home has a range of value, not a number. If you engaged multiple appraisers, you would receive multiple opinions that could vary widely. Here is a link to an article about home valuations that provides more information. A different appraiser may value the property above your purchase price.

- You paid for the appraisal, but the lender required it to help assess their risk. If the lender was satisfied with the appraiser’s opinion and agreed with the adjustment, they may simply approve the loan. Here is an article about appraisers making mistakes that may be helpful to you. I suspect you are well qualified to repay the loan based on your income, assets or the amount of the downpayment invested toward the purchase price.

- Did you tell the real estate agent, or the lender, or both of them the purchase of the home was contingent upon the appraiser’s opinion being equal to or greater than the purchase price at any time during your home search or loan pre-approval? If this conversation took place with the real estate agent, the request should have been included in the offer to purchase; if it was not, did both of you forget? It is more likely neither of you anticipated this event.

- In many areas of the country, real estate values are recovering well from the price meltdown debacle of a few years ago. Appraisers have latitude in judgment as to the weight of importance of a comparable sale when evaluating adjustments between comparables. When considering the many variables and comparables present in most markets the best choices and adjustments to the subject property can be problematic for an appraiser. If an appraiser can be convinced they erred, only the appraiser can make the call.

If you requested the home appraise for the purchase price and have an email or a verbal conversation witnessed by others, you may have a stronger argument. If not, or you were silent on this subject when asked to sign the purchase document, it may be too late.

You have several options

- Would you have countered to the seller if you could go back? Would you have countered for $176,000 or $179,000 (the appraiser corrected the appraisal, which indicates an error)? In the heat of potential competition for the house or the fear of the seller saying “no” over a small amount of the total purchase price can you know for certain what you would have done? Consider chalking this experience up to education and move on.

- Go back to the real estate company and communicate that you cannot accept their dismissal of your complaint. Seek to understand better what transpired, and now with this additional information, possibly attempt to negotiate for some relief.

- Seek an opinion from a competent real estate attorney. If you do not have an attorney here is a link to an article about how to find a competent attorney. You need to consider more information about the details. Only a review of the legal documents and the events that transpired can provide an informed opinion to understand your position fully.