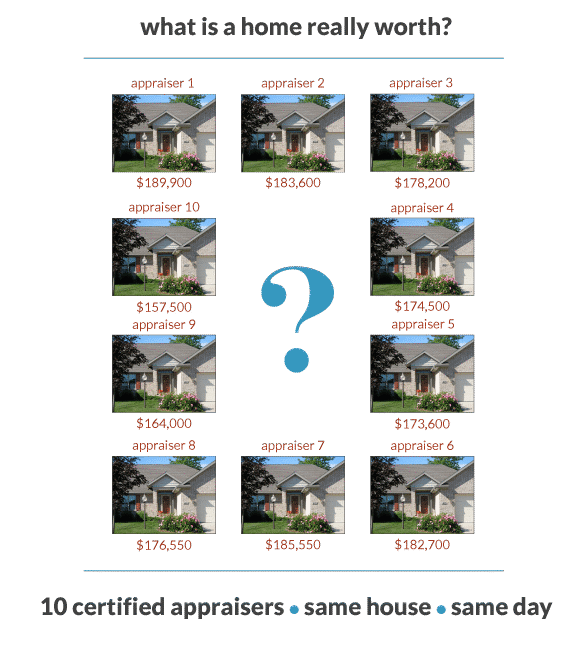

Reader Question: I have appraisal issues. I applied to an online lender a year ago to refinance my mortgage. The loan was approved. The only remaining step being the appraisal. The appraisal came in with a value that was woefully inadequate. The appraiser did not use fair comparables and neglected to perform due diligence in appraising the property. After six properties, I know a lot about valuation. Needless to say, I was furious and told them I was no longer interested in pursuing the refinancing.

I tried with the same online lender again in March 2016 and told them I wouldn’t accept the same appraiser. They assured me selection is a round-robin, and chances are slim the same appraiser would be selected. Well, I did get the same one and again pulled the refinancing.

I attempted again last month thinking this appraiser would not get called a third time. Their words were “It would be a statistical improbability.” It happened again! The lender attempted to remove the appraiser to no avail. I again pulled the refinancing, and the online lender is out. I need your help in figuring out how I can avoid getting the same appraiser a fourth time. What can I do?.

Monty’s Answer: There are two articles I have linked you to read for background before answering the question. One is about picking an appraiser, and the second article is about appraisal management companies (AMC’s). Reading these articles bring you up to date on the appraisal world.

Your letter lacked detail that may or may not affect the following advice, but, in a similar situation, here are two choices:

- Go to a lender that you can visit with face-to-face and apply for a loan. When you meet with the new lender, explain what happened and get their buy-in to your situation. When you get to the appraiser in the process, if it is the same one, do not grant the appointment – do not cancel the loan application. Call your new lender and tell them that what you feared would happen just happened again. Now your new lender can take this situation up with the AMC they are using.

- Go back to your current online lender. This time, when the originator answers the phone, ask to speak with their supervisor. Tell the supervisor you want their email address so you can communicate the problem you are having with the company in writing. Then send the letter you sent to me. Ask the supervisor to call you when they have reviewed the events. If they will not buy-in to helping solve the problem, you know where you stand. An option to this tactic is to ask the supervisor what can be done to avoid this appraiser. (Caution: the rules state the lender has no selection say, but the AMC’s are obligated to rotate appraisers. It is a gray area.)

It is unclear why you keep getting the same appraiser. Is your property located in a rural or a remote area? Is your property unique? Does your home contain one of the red flags of real estate? There are places in our country where it’s hard to find an appraiser, or possibly, the local appraisal community is choosing not to work with AMC’s.

There are also many AMC’s operating in the US. Find a lender that uses a different AMC. Is it possible that the appraiser has some relationship with this AMC? It is against the rules, but with three assignments on the same home back-to-back; maybe they found a way.

Because the rules evolve rapidly in a changing economy, it’s hard to be up-to-the-minute. I ran this answer past a senior high-volume mortgage lender, who added their bank will share the name of their AMC with a borrower, but every lender may have different policies.

Lastly, can you prove the appraiser is wrong? You state “The appraiser did not use fair comparables and neglected to perform due diligence in appraising the property.” Do you have better comparables? What did they miss in due diligence? Appraisers are paid for their opinion, they are not paid to agree with the property owner. Here is an article about challenging a home appraiser. You can help your situation by clearly demonstrating an error was made. Picking the wrong comparables is often problematic, but not counting 1000 square feet on the main floor is an easily verifiable mistake.